Ultra Supply & DemandThe "Ultra Supply & Demand" indicator is a sophisticated tool designed for traders looking to analyze market sentiment and potential price movements with a focus on supply and demand dynamics. It overlays on the chart to visually represent areas of supply and demand, providing insights into market liquidity levels and potential reversal points.

Dynamic Supply & Demand Zones: Automatically identifies and displays supply and demand zones based on trading volume and price action patterns. These zones are color-coded for easy identification and can be customized according to user preferences.

Volume-Based Analysis: Utilizes volume data to calculate supply and demand volumes, offering a deeper understanding of market strength behind these zones. Users can set a threshold for volume to filter out less significant signals.

Customizable Liquidation Levels: Offers three predefined liquidation level settings ("1st Touch," "Middle," "Fully") to help traders determine the depth of supply and demand zones. Users can also customize these settings to fit their trading strategy.

Real-time Updates: Continuously updates supply and demand zones as new bars form, ensuring that the information remains current and relevant throughout the trading session.

User-friendly Interface: Provides clear visual cues through color coding and labels, making it easier for traders to interpret the market conditions at a glance. Volume data can be displayed alongside the zones for added context.

Usage Instructions:

Add the Ultra Supply & Demand indicator to your chart.

Customize the indicator settings according to your trading style and preferences, including the display of volume, liquidation levels, and color schemes.

Observe the supply and demand zones on the chart. Look for divergences between price action and the indicator's zones as potential trade setups.

Combine the indicator with other technical analysis tools and indicators to confirm trade signals and enhance your decision-making process.

Tìm kiếm tập lệnh với "supply and demand"

Multiple Naked LevelsPURPOSE OF THE INDICATOR

This indicator autogenerates and displays naked levels and gaps of multiple types collected into one simple and easy to use indicator.

VALUE PROPOSITION OF THE INDICATOR AND HOW IT IS ORIGINAL AND USEFUL

1) CONVENIENCE : The purpose of this indicator is to offer traders with one coherent and robust indicator providing useful, valuable, and often used levels - in one place.

2) CLUSTERS OF CONFLUENCES : With this indicator it is easy to identify levels and zones on the chart with multiple confluences increasing the likelihood of a potential reversal zone.

THE TYPES OF LEVELS AND GAPS INCLUDED IN THE INDICATOR

The types of levels include the following:

1) PIVOT levels (Daily/Weekly/Monthly) depicted in the chart as: dnPIV, wnPIV, mnPIV.

2) POC (Point of Control) levels (Daily/Weekly/Monthly) depicted in the chart as: dnPoC, wnPoC, mnPoC.

3) VAH/VAL STD 1 levels (Value Area High/Low with 1 std) (Daily/Weekly/Monthly) depicted in the chart as: dnVAH1/dnVAL1, wnVAH1/wnVAL1, mnVAH1/mnVAL1

4) VAH/VAL STD 2 levels (Value Area High/Low with 2 std) (Daily/Weekly/Monthly) depicted in the chart as: dnVAH2/dnVAL2, wnVAH2/wnVAL2, mnVAH1/mnVAL2

5) FAIR VALUE GAPS (Daily/Weekly/Monthly) depicted in the chart as: dnFVG, wnFVG, mnFVG.

6) CME GAPS (Daily) depicted in the chart as: dnCME.

7) EQUILIBRIUM levels (Daily/Weekly/Monthly) depicted in the chart as dnEQ, wnEQ, mnEQ.

HOW-TO ACTIVATE LEVEL TYPES AND TIMEFRAMES AND HOW-TO USE THE INDICATOR

You can simply choose which of the levels to be activated and displayed by clicking on the desired radio button in the settings menu.

You can locate the settings menu by clicking into the Object Tree window, left-click on the Multiple Naked Levels and select Settings.

You will then get a menu of different level types and timeframes. Click the checkboxes for the level types and timeframes that you want to display on the chart.

You can then go into the chart and check out which naked levels that have appeared. You can then use those levels as part of your technical analysis.

The levels displayed on the chart can serve as additional confluences or as part of your overall technical analysis and indicators.

In order to back-test the impact of the different naked levels you can also enable tapped levels to be depicted on the chart. Do this by toggling the 'Show tapped levels' checkbox.

Keep in mind however that Trading View can not shom more than 500 lines and text boxes so the indocator will not be able to give you the complete history back to the start for long duration assets.

In order to clean up the charts a little bit there are two additional settings that can be used in the Settings menu:

- Selecting the price range (%) from the current price to be included in the chart. The default is 25%. That means that all levels below or above 20% will not be displayed. You can set this level yourself from 0 up to 100%.

- Selecting the minimum gap size to include on the chart. The default is 1%. That means that all gaps/ranges below 1% in price difference will not be displayed on the chart. You can set the minimum gap size yourself.

BASIC DESCRIPTION OF THE INNER WORKINGS OF THE INDICTATOR

The way the indicator works is that it calculates and identifies all levels from the list of levels type and timeframes above. The indicator then adds this level to a list of untapped levels.

Then for each bar after, it checks if the level has been tapped. If the level has been tapped or a gap/range completely filled, this level is removed from the list so that the levels displayed in the end are only naked/untapped levels.

Below is a descrition of each of the level types and how it is caluclated (algorithm):

PIVOT

Daily, Weekly and Monthly levels in trading refer to significant price points that traders monitor within the context of a single trading day. These levels can provide insights into market behavior and help traders make informed decisions regarding entry and exit points.

Traders often use D/W/M levels to set entry and exit points for trades. For example, entering long positions near support (daily close) or selling near resistance (daily close).

Daily levels are used to set stop-loss orders. Placing stops just below the daily close for long positions or above the daily close for short positions can help manage risk.

The relationship between price movement and daily levels provides insights into market sentiment. For instance, if the price fails to break above the daily high, it may signify bearish sentiment, while a strong breakout can indicate bullish sentiment.

The way these levels are calculated in this indicator is based on finding pivots in the chart on D/W/M timeframe. The level is then set to previous D/W/M close = current D/W/M open.

In addition, when price is going up previous D/W/M open must be smaller than previous D/W/M close and current D/W/M close must be smaller than the current D/W/M open. When price is going down the opposite.

POINT OF CONTROL

The Point of Control (POC) is a key concept in volume profile analysis, which is commonly used in trading.

It represents the price level at which the highest volume of trading occurred during a specific period.

The POC is derived from the volume traded at various price levels over a defined time frame. In this indicator the timeframes are Daily, Weekly, and Montly.

It identifies the price level where the most trades took place, indicating strong interest and activity from traders at that price.

The POC often acts as a significant support or resistance level. If the price approaches the POC from above, it may act as a support level, while if approached from below, it can serve as a resistance level. Traders monitor the POC to gauge potential reversals or breakouts.

The way the POC is calculated in this indicator is by an approximation by analysing intrabars for the respective timeperiod (D/W/M), assigning the volume for each intrabar into the price-bins that the intrabar covers and finally identifying the bin with the highest aggregated volume.

The POC is the price in the middle of this bin.

The indicator uses a sample space for intrabars on the Daily timeframe of 15 minutes, 35 minutes for the Weekly timeframe, and 140 minutes for the Monthly timeframe.

The indicator has predefined the size of the bins to 0.2% of the price at the range low. That implies that the precision of the calulated POC og VAH/VAL is within 0.2%.

This reduction of precision is a tradeoff for performance and speed of the indicator.

This also implies that the bigger the difference from range high prices to range low prices the more bins the algorithm will iterate over. This is typically the case when calculating the monthly volume profile levels and especially high volatility assets such as alt coins.

Sometimes the number of iterations becomes too big for Trading View to handle. In these cases the bin size will be increased even more to reduce the number of iterations.

In such cases the bin size might increase by a factor of 2-3 decreasing the accuracy of the Volume Profile levels.

Anyway, since these Volume Profile levels are approximations and since precision is traded for performance the user should consider the Volume profile levels(POC, VAH, VAL) as zones rather than pin point accurate levels.

VALUE AREA HIGH/LOW STD1/STD2

The Value Area High (VAH) and Value Area Low (VAL) are important concepts in volume profile analysis, helping traders understand price levels where the majority of trading activity occurs for a given period.

The Value Area High/Low is the upper/lower boundary of the value area, representing the highest price level at which a certain percentage of the total trading volume occurred within a specified period.

The VAH/VAL indicates the price point above/below which the majority of trading activity is considered less valuable. It can serve as a potential resistance/support level, as prices above/below this level may experience selling/buying pressure from traders who view the price as overvalued/undervalued

In this indicator the timeframes are Daily, Weekly, and Monthly. This indicator provides two boundaries that can be selected in the menu.

The first boundary is 70% of the total volume (=1 standard deviation from mean). The second boundary is 95% of the total volume (=2 standard deviation from mean).

The way VAH/VAL is calculated is based on the same algorithm as for the POC.

However instead of identifying the bin with the highest volume, we start from range low and sum up the volume for each bin until the aggregated volume = 30%/70% for VAL1/VAH1 and aggregated volume = 5%/95% for VAL2/VAH2.

Then we simply set the VAL/VAH equal to the low of the respective bin.

FAIR VALUE GAPS

Fair Value Gaps (FVG) is a concept primarily used in technical analysis and price action trading, particularly within the context of futures and forex markets. They refer to areas on a price chart where there is a noticeable lack of trading activity, often highlighted by a significant price movement away from a previous level without trading occurring in between.

FVGs represent price levels where the market has moved significantly without any meaningful trading occurring. This can be seen as a "gap" on the price chart, where the price jumps from one level to another, often due to a rapid market reaction to news, events, or other factors.

These gaps typically appear when prices rise or fall quickly, creating a space on the chart where no transactions have taken place. For example, if a stock opens sharply higher and there are no trades at the prices in between the two levels, it creates a gap. The areas within these gaps can be areas of liquidity that the market may return to “fill” later on.

FVGs highlight inefficiencies in pricing and can indicate areas where the market may correct itself. When the market moves rapidly, it may leave behind price levels that traders eventually revisit to establish fair value.

Traders often watch for these gaps as potential reversal or continuation points. Many traders believe that price will eventually “fill” the gap, meaning it will return to those price levels, providing potential entry or exit points.

This indicator calculate FVGs on three different timeframes, Daily, Weekly and Montly.

In this indicator the FVGs are identified by looking for a three-candle pattern on a chart, signalling a discrete imbalance in order volume that prompts a quick price adjustment. These gaps reflect moments where the market sentiment strongly leans towards buying or selling yet lacks the opposite orders to maintain price stability.

The indicator sets the gap to the difference from the high of the first bar to the low of the third bar when price is moving up or from the low of the first bar to the high of the third bar when price is moving down.

CME GAPS (BTC only)

CME gaps refer to price discrepancies that can occur in charts for futures contracts traded on the Chicago Mercantile Exchange (CME). These gaps typically arise from the fact that many futures markets, including those on the CME, operate nearly 24 hours a day but may have significant price movements during periods when the market is closed.

CME gaps occur when there is a difference between the closing price of a futures contract on one trading day and the opening price on the following trading day. This difference can create a "gap" on the price chart.

Opening Gaps: These usually happen when the market opens significantly higher or lower than the previous day's close, often influenced by news, economic data releases, or other market events occurring during non-trading hours.

Gaps can result from reactions to major announcements or developments, such as earnings reports, geopolitical events, or changes in economic indicators, leading to rapid price movements.

The importance of CME Gaps in Trading is the potential for Filling Gaps: Many traders believe that prices often "fill" gaps, meaning that prices may return to the gap area to establish fair value.

This can create potential trading opportunities based on the expectation of gap filling. Gaps can act as significant support or resistance levels. Traders monitor these levels to identify potential reversal points in price action.

The way the gap is identified in this indicator is by checking if current open is higher than previous bar close when price is moving up or if current open is lower than previous day close when price is moving down.

EQUILIBRIUM

Equilibrium in finance and trading refers to a state where supply and demand in a market balance each other, resulting in stable prices. It is a key concept in various economic and trading contexts. Here’s a concise description:

Market Equilibrium occurs when the quantity of a good or service supplied equals the quantity demanded at a specific price level. At this point, there is no inherent pressure for the price to change, as buyers and sellers are in agreement.

Equilibrium Price is the price at which the market is in equilibrium. It reflects the point where the supply curve intersects the demand curve on a graph. At the equilibrium price, the market clears, meaning there are no surplus goods or shortages.

In this indicator the equilibrium level is calculated simply by finding the midpoint of the Daily, Weekly, and Montly candles respectively.

NOTES

1) Performance. The algorithms are quite resource intensive and the time it takes the indicator to calculate all the levels could be 5 seconds or more, depending on the number of bars in the chart and especially if Montly Volume Profile levels are selected (POC, VAH or VAL).

2) Levels displayed vs the selected chart timeframe. On a timeframe smaller than the daily TF - both Daily, Weekly, and Monthly levels will be displayed. On a timeframe bigger than the daily TF but smaller than the weekly TF - the Weekly and Monthly levels will be display but not the Daily levels. On a timeframe bigger than the weekly TF but smaller than the monthly TF - only the Monthly levels will be displayed. Not Daily and Weekly.

CREDITS

The core algorithm for calculating the POC levels is based on the indicator "Naked Intrabar POC" developed by rumpypumpydumpy (https:www.tradingview.com/u/rumpypumpydumpy/).

The "Naked intrabar POC" indicator calculates the POC on the current chart timeframe.

This indicator (Multiple Naked Levels) adds two new features:

1) It calculates the POC on three specific timeframes, the Daily, Weekly, and Monthly timeframes - not only the current chart timeframe.

2) It adds functionaly by calculating the VAL and VAH of the volume profile on the Daily, Weekly, Monthly timeframes .

RedK_Supply/Demand Volume Viewer v1Background

============

VolumeViewer is a volume indicator, that offers a simple way to estimate the movement and balance (or lack of) of supply & demand volume based on the shape of the price bar. i put this together few years ago and i have a version of this published for another platform under different names (Directional Volume, BetterVolume) in case you come across them

what is V.Viewer

=====================

The idea here is to find a "simple proxy" for estimating the demand or supply portions of a volume bar - these 2 forces have the potential to affect the current price trend so we want an easy way to track them - or to understand if a stock is in accumulation or distribution - we want to do this without having access to Level II or bid/ask data, and without having to get into the complexity of exploring the lower timeframe price & volume data

- to achieve that, we depend on a simple assumption, that the volume associated with an up move is "demand" and the volume associated with a down move is "Supply". so we basically extrapolate these supply and demand values based on how the bar looks like - a full "green" price bar / candle will be considered 100% demand, and a full "red" price bar will be considered 100% supply - a bar that opens and closes at the same level will be 50/50 split between supply & demand.

- you may say this is a "too simple" of an assumption to make, but believe me, it works :) at least at the basic scenario we need here: i'm just exploring the volume movement and finding key levels - and it provides a good improvement compared to the classic way we see volume on a chart - which is still available here in VolumeViewer.

in all cases, i consider this to be work in progress, so i'd welcome any ideas to improve (without getting too complicated) - there's already a host of great volume-based indicators that will do the multi timeframe drill down, but that's not my scope here.

Technical Jargon & calculation

===========================

1. first we calculate a score % for the volume portion that is considered demand based on the bar shape

skip this part if it sounds too technical => if you're into coding indicators, you would probably know there are couple of different concepts for that algorithm - for example, the one used in Balance Of Power formula - which i'm a big fan of - but the one i use here is different. (how?) this is my own, ant it simply applies double weight for the "wick" parts of a price bar compared to the "body of the bar" -- i did some side-by-side comparison in past and decided this one works better. you can change it in the code if you like

2. after calculating the Bull vs Bears portion of volume, we take a moving average of both for the length you set, to come up with what we consider to be the Demand vs Supply - as usual, i use a weighted moving average (WMA) here.

3. the balance or net volume between these 2 lines is calculated, then we apply a final smoothing and that's the main plot we will get

4. being a very visual person, i did my best to build up the visuals in the correct order - then also to ensure the "study title" bar is properly organized and is simple and useful (Full Volume, Supply, Demand, Net Volume).

- i wish there was a way in Pine to hide a value that i still need to visually plot but don't want it showing its value on the study title bar, but couldn't find it. so the last plot value is repeated twice.

How to use

===========

- V.Viewer is set up to show the simplified view by default for simplicity. so when you first add it to a chart, you will get only the supply vs demand view you can see in the middle pane in the above chart

- Optional / detailed mode: go into the settings, and expose all other plots, you will be able to add the classic volume histogram, and the Supply / Demand lines - note these 2 lines will be overlay-ed on top of each other - this provides an easy way to see who is in control - especially if you change the display of these 2 lines into "area" style. This is what is showing in the lower pane in the above chart.

** Exploring Key Price Levels

- the premise is, at spots where there's big lack of balance, that's where to expect to find key price levels (support / resistance) and these price levels will come into play in future so can be used to set entry / exit targets for our trades - see the example in the AAPL chart where you can easily locate these "balance or reversal levels" using the tops/bottoms/zero-crossings from the Net Volume line

** Use for longer-term Price Analysis

- we can also use this simple indicator to gain more insights (at a high level) of the price in terms of accumulation vs distribution and if the sellers or buyers are in control - for example, in the above AAPL chart, V.Viewer tells us that buyers have been in control since October 19 - even during the recent drop, demand continued to be in play - compare that to DIS chart below for the same period, where it shows that the market was dumping DIS thru the weakness. DIS was bleeding red most of the time

Final thoughts

=============

- V.Viewer is an attempt to enhance the way we see and use Volume by leveraging the shape of the price bar to estimate volume supply & demand - and the Net between the 2

- it will work for stocks and other instruments as long as there's volume data

- note that V.Viewer does not track trend. each bar is taken in isolation of prior bars - the price may be going down and V.Viewer is showing supply going up (absorption scenario?) - so i suggest you do not use it to make decisions without consulting other trend / momentum indicators - of course this is a possible improvement idea, or can be implemented in another indicator, add in trend somehow, or maybe think of making this a +100 / -100 Oscillator .. feel free to play with these thoughts

- all thoughts welcome - if this is useful to you in your trading, please share with other trades here to learn from each other

- the code is commented - please feel free to use it as you like, or build things on top of it - but please continue to credit the author of this code :)

good luck!

-

Support Resistance Major/Minor [TradingFinder] Market Structure🔵 Introduction

Support and resistance levels are key concepts in technical analysis, serving as critical points where prices pause or reverse due to the interaction of supply and demand. These foundational elements in price action and classical technical analysis assist traders in understanding market behavior and making better trading decisions.

Support levels are zones where demand is strong enough to prevent further price declines, while resistance levels act as barriers that hinder price increases.

Support and resistance levels are divided into two main types: static and dynamic. Static levels are fixed horizontal lines on charts, formed based on historical price points, and are crucial due to repeated price reactions in these areas.

Dynamic levels, on the other hand, move with market trends and are often identified using tools like moving averages and trendlines. These levels are particularly useful for analyzing dynamic trends and identifying potential reversal points in financial markets.

The importance of support and resistance in technical analysis lies in their ability to pinpoint price reversal or continuation points. Professional traders use these levels to determine optimal entry and exit points and combine them with tools such as Fibonacci retracements or moving averages for precise strategies.

Detailed analysis of price behavior at these levels provides insights into trend strength and the likelihood of price breaks or reversals. By understanding these concepts, technical analysts can forecast future price movements and optimize their trading decisions using tools such as indicators and price action. Support and resistance levels, as a cornerstone of technical analysis, form the foundation for many trading strategies.

🔵 How to Use

The Static Support and Resistance Indicator is a vital tool for identifying significant price zones in financial markets. It automatically detects major and minor support and resistance levels in both short-term and long-term intervals, enabling traders to analyze price behavior accurately and develop optimal entry and exit strategies.

🟣 Major Long-Term Support and Resistance

Major Long-Term Support : The lowest price points recorded over long-term intervals that prevent further declines.

Major Long-Term Resistance : The highest price points in long-term intervals that limit further price increases.

🟣 Minor Long-Term Support and Resistance

Minor Long-Term Support : Temporary halts in price decline within a downtrend over long-term intervals.

Minor Long-Term Resistance : Short-term zones within long-term intervals where prices react negatively in an uptrend.

🟣 Major Short-Term Support and Resistance

Major Short-Term Support : The lowest price points in short-term intervals that act as barriers against sharp price drops.

Major Short-Term Resistance : The highest points in short-term intervals that prevent further price surges.

🟣 Minor Short-Term Support and Resistance

Minor Short-Term Support : Temporary halts in price decline within short-term downtrends.

Minor Short-Term Resistance : Zones where price reacts quickly and reverses in short-term uptrends.

🔵 Settings

Long Term S&R Pivot Period : Defines the interval for identifying long-term support and resistance levels (default: 21).

Short Term S&R Pivot Period : Defines the interval for identifying short-term support and resistance levels (default: 5).

🟣 Long-Term Lines

Major Line Display : Enable/disable major long-term lines.

Minor Line Display : Enable/disable minor long-term lines.

Major Line Colors : Green for support, red for resistance (long-term major levels).

Minor Line Colors : Light green for support, light red for resistance (long-term minor levels).

Major Line Style : Choose between solid, dotted, or dashed lines for major long-term levels.

Minor Line Style : Choose between solid, dotted, or dashed lines for minor long-term levels.

Major Line Width : Adjust the thickness of major long-term lines.

Minor Line Width : Adjust the thickness of minor long-term lines.

🟣 Short-Term Lines

Major Line Display : Enable/disable major short-term lines.

Minor Line Display : Enable/disable minor short-term lines.

Major Line Colors : Gray-green for support, gray-red for resistance (short-term major levels).

Minor Line Colors : Dark green for support, dark red for resistance (short-term minor levels).

Major Line Style : Choose between solid, dotted, or dashed lines for major short-term levels.

Minor Line Style : Choose between solid, dotted, or dashed lines for minor short-term levels.

Major Line Width : Adjust the thickness of major short-term lines.

Minor Line Width : Adjust the thickness of minor short-term lines.

🔵 Conclusion

Static support and resistance levels are among the most critical tools in technical analysis, helping traders identify key reversal or continuation points.

This indicator simplifies and enhances the analysis process by automatically detecting major and minor levels in both short-term and long-term intervals. It allows traders to customize settings to suit their trading strategies and analyze different market levels effectively.

Using this indicator improves price action analysis, enhances market understanding, and identifies trading opportunities. Applicable to all trading styles, from day trading to long-term investing, it is an essential tool for technical analysis.

Combining this indicator with other tools like trendlines, Fibonacci retracements, and moving averages enables comprehensive analysis and allows traders to navigate financial markets with greater confidence.

Indecisive and Explosive CandlesThe Explosive & Base Candle with Gaps Identifier is an indicator designed to enhance your market analysis by identifying critical candle types and gaps in price action. This tool aids traders in pinpointing zones of significant buyer-seller interaction and potential institutional activity, providing valuable insights for strategic trading decisions.

Main Features:

Base Candle Identification: This feature detects Base candles, also known as indecisive candles, within the price action. A Base candle is characterized by a body (the difference between the close and open prices) that is less than or equal to 50% of its total range (the difference between the high and low prices). These candles mark zones where buyers and sellers are evenly matched, highlighting areas of potential support and resistance.

Explosive Candle Identification: The indicator identifies Explosive candles, which are indicative of strong market moves often driven by institutional activity. An Explosive candle is defined by a body that is greater than 70% of its total range. Recognizing these candles helps traders spot significant momentum and potential breakout points.

Supply and Demand Zone Identification: Both Base and Explosive candles are essential for identifying supply and demand zones within the price action. These zones are crucial for traders to place their trades based on the likelihood of price reversals or continuations.

Gap Detection: The indicator also detects gaps, defined as the difference between the close price of one candle and the open price of the next. Gaps are significant because prices often return to these levels to "fill the gap," providing opportunities for traders to predict price movements and place strategic trades.

Visual Markings and Alerts: The indicator visually marks Base and Explosive candles as well as gaps directly on the chart, making them easily identifiable at a glance. Traders can also set customizable alerts to notify them when these key candle types and gaps appear, ensuring they never miss an important trading opportunity.

Customizable Settings: Tailor the indicator’s settings to match your trading style and preferences. Adjust the criteria for Base and Explosive candles, as well as how gaps are detected and displayed, to suit your specific analysis needs.

How to Use:

Add the Indicator: Apply the Explosive & Base Candle with Gaps Identifier to your TradingView chart.

Analyze Identified Zones: Observe the marked Base and Explosive candles and gaps to identify key areas of support, resistance, and potential price reversals or continuations.

Set Alerts: Customize and set alerts for the detection of Base candles, Explosive candles, and gaps to stay informed of critical market movements in real-time.

Integrate with Your Strategy: Use the insights provided by the indicator to enhance your existing trading strategy, improving your entry and exit points based on the identified supply and demand zones.

The Explosive & Base Candle with Gaps Identifier is an invaluable tool for traders aiming to refine their market analysis and make more informed trading decisions. By identifying critical areas of price action, this indicator supports traders in navigating the complexities of the financial markets with greater precision and confidence.

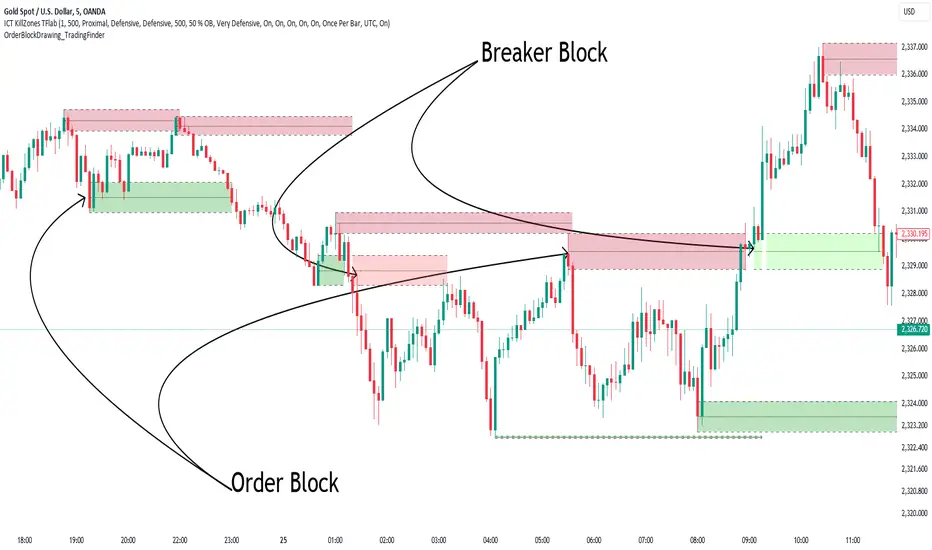

Order Block Drawing [TradingFinder]🔵 Introduction

Perhaps one of the most challenging tasks for Pine script developers (especially beginners) is properly drawing order blocks. While utilizing the latest technical analysis methods for "Price Action," beginners heavily rely on accurately plotting "Supply" and "Demand" zones, following concepts like "Smart Money Concept" and "ICT".

However, drawing "Order Blocks" may pose a challenge for developers. Therefore, to minimize bugs, increase accuracy, and speed up the process of coding order blocks, we have released the "Order Block Drawing" library.

Below, you can read more details about how to use this library.

Important :

This library has direct and indirect outputs. The indirect output includes the ranges of order blocks plotted on the chart. However, the direct output is a "Boolean" value that becomes "true" only when the price touches an order block, colloquially termed as "Mitigate." You can use this output for setting up alerts.

🔵 How to Use

First, you can add the library to your code as shown in the example below.

import TFlab/OrderBlockDrawing_TradingFinder/1

🟣Parameters

OBDrawing(OBType, TriggerCondition, DistalPrice, ProximalPrice, Index, OBValidDis, Show, ColorZone) =>

Parameters:

• OBType (string)

• TriggerCondition (bool)

• DistalPrice (float)

• ProximalPrice (float)

• Index (int)

• OBValidDis (int)

• Show (bool)

• ColorZone (color)

OBType : All order blocks are summarized into two types: "Supply" and "Demand." You should input your order block type in this parameter. Enter "Demand" for drawing demand zones and "Supply" for drawing supply zones.

TriggerCondition : Input the condition under which you want the order block to be drawn in this parameter.

DistalPrice : Generally, if each zone is formed by two lines, the farthest line from the price is termed "Distal." This input receives the price of the "Distal" line.

ProximalPrice : Generally, if each zone is formed by two lines, the nearest line to the price is termed "Proximal" line.

Index : This input receives the value of the "bar_index" at the beginning of the order block. You should store the "bar_index" value at the occurrence of the condition for the order block to be drawn and input it here.

OBValidDis : Order blocks continue to be drawn until a new order block is drawn or the order block is "Mitigate." You can specify how many candles after their initiation order blocks should continue. If you want no limitation, enter the number 4998.

Show : You may need to manage whether to display or hide order blocks. When this input is "On", order blocks are displayed, and when it's "Off", order blocks are not displayed.

ColorZone : You can input your preferred color for drawing order blocks.

🔵 Function Outputs

This function has only one output. This output is of type "Boolean" and becomes "true" only when the price touches an order block. Each order block can be touched only once and then loses its validity. You can use this output for alerts.

= Drawing.OBDrawing('Demand', Condition, Distal, Proximal, Index, 4998, true, Color)

Institutional Supply and Demand ZonesThis indicator aims to identify price levels where institutional investors have positioned their buy or sell orders. These buy orders establish "demand zones," while sell orders create "supply zones." Identifying these zones enables us to anticipate potential reversals in price trends, allowing us to profitably engage in these significant market movements alongside major institutions. These zones are formed when price action goes from balanced to imbalanced. These zones are based on orders. Unlike standard support and resistance levels, when price breaks below a demand zone or above a supply zone, these zones disappear from the chart.

Supply is formed by a green candle followed by a major red candle that is at least double the size of previous green candle. The zone is then charted from the open of the green candle to the highest point in the candle. Vice versa for a demand zone (red into green).

These zones are traded by:

1. Look for a volume spike in a zone

2. A trend/trendline break out of the zone

Order Block Overlapping Drawing [TradingFinder]🔵 Introduction

Technical analysis is a fundamental tool in financial markets, helping traders identify key areas on price charts to make informed trading decisions. The ICT (Inner Circle Trader) style, developed by Michael Huddleston, is one of the most advanced methods in this field.

It enables traders to precisely identify and exploit critical zones such as Order Blocks, Breaker Blocks, Fair Value Gaps (FVGs), and Inversion Fair Value Gaps (IFVGs).

To streamline and simplify the use of these key areas, a library has been developed in Pine Script, the scripting language for the TradingView platform. This library allows you to automatically detect overlapping zones between Order Blocks and other similar areas, and visually display them on your chart.

This tool is particularly useful for creating indicators like Balanced Price Range (BPR) and ICT Unicorn Model.

🔵 How to Use

This section explains how to use the Pine Script library. This library assists you in easily identifying and analyzing overlapping areas between Order Blocks and other zones, such as Breaker Blocks and Fair Value Gaps.

To add "Order Block Overlapping Drawing", you must first add the following code to your script.

import TFlab/OrderBlockOverlappingDrawing/1

🟣 Inputs

The library includes the "OBOverlappingDrawing" function, which you can use to detect and display overlapping zones. This function identifies and draws overlapping zones based on the Order Block type, trigger conditions, previous and current prices, and other relevant parameters.

🟣 Parameters

OBOverlappingDrawing(OBType , TriggerConditionOrigin, distalPrice_Pre, proximalPrice_Pre , distalPrice_Curr, proximalPrice_Curr, Index_Curr , OBValidGlobal, OBValidDis, MitigationLvL, ShowAll, Show, ColorZone) =>

OBType (string)

TriggerConditionOrigin (bool)

distalPrice_Pre (float)

proximalPrice_Pre (float)

distalPrice_Curr (float)

proximalPrice_Curr (float)

Index_Curr (int)

OBValidGlobal (bool)

OBValidDis (int)

MitigationLvL (string)

ShowAll (bool)

Show (bool)

ColorZone (color)

In this example, various parameters are defined to detect overlapping zones and draw them on the chart. Based on these settings, the overlapping areas will be automatically drawn on the chart.

OBType : All order blocks are summarized into two types: "Supply" and "Demand." You should input your Current order block type in this parameter. Enter "Demand" for drawing demand zones and "Supply" for drawing supply zones.

TriggerConditionOrigin : Input the condition under which you want the Current order block to be drawn in this parameter.

distalPrice_Pre : Generally, if each zone is formed by two lines, the farthest line from the price is termed Pervious "Distal." This input receives the price of the "Distal" line.

proximalPrice_Pre : Generally, if each zone is formed by two lines, the nearest line to the price is termed Previous "Proximal" line.

distalPrice_Curr : Generally, if each zone is formed by two lines, the farthest line from the price is termed Current "Distal." This input receives the price of the "Distal" line.

proximalPrice_Curr : Generally, if each zone is formed by two lines, the nearest line to the price is termed Current "Proximal" line.

Index_Curr : This input receives the value of the "bar_index" at the beginning of the order block. You should store the "bar_index" value at the occurrence of the condition for the Current order block to be drawn and input it here.

OBValidGlobal : This parameter is a boolean in which you can enter the condition that you want to execute to stop drawing the block order. If you do not have a special condition, you should set it to True.

OBValidDis : Order blocks continue to be drawn until a new order block is drawn or the order block is "Mitigate." You can specify how many candles after their initiation order blocks should continue. If you want no limitation, enter the number 4998.

MitigationLvL : This parameter is a string. Its inputs are one of "Proximal", "Distal" or "50 % OB" modes, which you can enter according to your needs. The "50 % OB" line is the middle line between distal and proximal.

ShowAll : This is a boolean parameter, if it is "true" the entire order of blocks will be displayed, and if it is "false" only the last block order will be displayed.

Show : You may need to manage whether to display or hide order blocks. When this input is "On", order blocks are displayed, and when it's "Off", order blocks are not displayed.

ColorZone : You can input your preferred color for drawing order blocks.

🟣 Output

Mitigation Alerts : This library allows you to leverage Mitigation Alerts to detect specific conditions that could lead to trend reversals. These alerts help you react promptly in your trades, ensuring better management of market shifts.

🔵 Conclusion

The Pine Script library provided is a powerful tool for technical analysis, especially in the ICT style. It enables you to detect overlapping zones between Order Blocks and other significant areas like Breaker Blocks and Fair Value Gaps, improving your trading strategies. By utilizing this tool, you can perform more precise analysis and manage risks effectively in your trades.

HDT CloudsHDT Clouds combines custom clouds such as the 200EMA/MA cloud indicator to create high confluence bounce zones when combined with VWAP. The HDT indicator combines various clouds with the Volume Weighted Average Price indicator and Standard Deviations which allow users to identify areas on the chart where the stock may reverse.

On smaller time frames, like the 5/15/30minute, the 200ema/ma cloud and VWAP (when sitting in the same relative area) creates pockets of supply or demand.

In addition, the various moving average clouds, such as the 8/9ema cloud and the 34/50ema cloud, create areas of supply and demand depending on the overall trend. If the stock is trending very strongly to the upside, the 8/9ema can be used as a potential bounce area. Whereas, if the stock is trending, but not quite as strong, the stock may have demand at the 34-50ema where the stock could see a potential bounce to the upside. What sets this indicator apart from other moving average clouds is the incorporation of VWAP/Standard Deviation and the combining of a 200EMA/MA indicator which creates a strong pocket of demand even on lower time frames such as the 5 or 15 minute time frame.

Volatility Risk Premium GOLD & SILVER 1.0ENGLISH

This indicator (V-R-P) calculates the (one month) Volatility Risk Premium for GOLD and SILVER.

V-R-P is the premium hedgers pay for over Realized Volatility for GOLD and SILVER options.

The premium stems from hedgers paying to insure their portfolios, and manifests itself in the differential between the price at which options are sold (Implied Volatility) and the volatility GOLD and SILVER ultimately realize (Realized Volatility).

I am using 30-day Implied Volatility (IV) and 21-day Realized Volatility (HV) as the basis for my calculation, as one month of IV is based on 30 calendaristic days and one month of HV is based on 21 trading days.

At first, the indicator appears blank and a label instructs you to choose which index you want the V-R-P to plot on the chart. Use the indicator settings (the sprocket) to choose one of the precious metals (or both).

Together with the V-R-P line, the indicator will show its one year moving average within a range of +/- 15% (which you can change) for benchmarking purposes. We should consider this range the “normalized” V-R-P for the actual period.

The Zero Line is also marked on the indicator.

Interpretation

When V-R-P is within the “normalized” range, … well... volatility and uncertainty, as it’s seen by the option market, is “normal”. We have a “premium” of volatility which should be considered normal.

When V-R-P is above the “normalized” range, the volatility premium is high. This means that investors are willing to pay more for options because they see an increasing uncertainty in markets.

When V-R-P is below the “normalized” range but positive (above the Zero line), the premium investors are willing to pay for risk is low, meaning they see decreasing uncertainty and risks in the market, but not by much.

When V-R-P is negative (below the Zero line), we have COMPLACENCY. This means investors see upcoming risk as being lower than what happened in the market in the recent past (within the last 30 days).

CONCEPTS :

Volatility Risk Premium

The volatility risk premium (V-R-P) is the notion that implied volatility (IV) tends to be higher than realized volatility (HV) as market participants tend to overestimate the likelihood of a significant market crash.

This overestimation may account for an increase in demand for options as protection against an equity portfolio. Basically, this heightened perception of risk may lead to a higher willingness to pay for these options to hedge a portfolio.

In other words, investors are willing to pay a premium for options to have protection against significant market crashes even if statistically the probability of these crashes is lesser or even negligible.

Therefore, the tendency of implied volatility is to be higher than realized volatility, thus V-R-P being positive.

Realized/Historical Volatility

Historical Volatility (HV) is the statistical measure of the dispersion of returns for an index over a given period of time.

Historical volatility is a well-known concept in finance, but there is confusion in how exactly it is calculated. Different sources may use slightly different historical volatility formulas.

For calculating Historical Volatility I am using the most common approach: annualized standard deviation of logarithmic returns, based on daily closing prices.

Implied Volatility

Implied Volatility (IV) is the market's forecast of a likely movement in the price of the index and it is expressed annualized, using percentages and standard deviations over a specified time horizon (usually 30 days).

IV is used to price options contracts where high implied volatility results in options with higher premiums and vice versa. Also, options supply and demand and time value are major determining factors for calculating Implied Volatility.

Implied Volatility usually increases in bearish markets and decreases when the market is bullish.

For determining GOLD and SILVER implied volatility I used their volatility indices: GVZ and VXSLV (30-day IV) provided by CBOE.

Warning

Please be aware that because CBOE doesn’t provide real-time data in Tradingview, my V-R-P calculation is also delayed, so you shouldn’t use it in the first 15 minutes after the opening.

This indicator is calibrated for a daily time frame.

----------------------------------------------------------------------

ESPAŇOL

Este indicador (V-R-P) calcula la Prima de Riesgo de Volatilidad (de un mes) para GOLD y SILVER.

V-R-P es la prima que pagan los hedgers sobre la Volatilidad Realizada para las opciones de GOLD y SILVER.

La prima proviene de los hedgers que pagan para asegurar sus carteras y se manifiesta en el diferencial entre el precio al que se venden las opciones (Volatilidad Implícita) y la volatilidad que finalmente se realiza en el ORO y la PLATA (Volatilidad Realizada).

Estoy utilizando la Volatilidad Implícita (IV) de 30 días y la Volatilidad Realizada (HV) de 21 días como base para mi cálculo, ya que un mes de IV se basa en 30 días calendario y un mes de HV se basa en 21 días de negociación.

Al principio, el indicador aparece en blanco y una etiqueta le indica que elija qué índice desea que el V-R-P represente en el gráfico. Use la configuración del indicador (la rueda dentada) para elegir uno de los metales preciosos (o ambos).

Junto con la línea V-R-P, el indicador mostrará su promedio móvil de un año dentro de un rango de +/- 15% (que puede cambiar) con fines de evaluación comparativa. Deberíamos considerar este rango como el V-R-P "normalizado" para el período real.

La línea Cero también está marcada en el indicador.

Interpretación

Cuando el V-R-P está dentro del rango "normalizado",... bueno... la volatilidad y la incertidumbre, como las ve el mercado de opciones, es "normal". Tenemos una “prima” de volatilidad que debería considerarse normal.

Cuando V-R-P está por encima del rango "normalizado", la prima de volatilidad es alta. Esto significa que los inversores están dispuestos a pagar más por las opciones porque ven una creciente incertidumbre en los mercados.

Cuando el V-R-P está por debajo del rango "normalizado" pero es positivo (por encima de la línea Cero), la prima que los inversores están dispuestos a pagar por el riesgo es baja, lo que significa que ven una disminución, pero no pronunciada, de la incertidumbre y los riesgos en el mercado.

Cuando V-R-P es negativo (por debajo de la línea Cero), tenemos COMPLACENCIA. Esto significa que los inversores ven el riesgo próximo como menor que lo que sucedió en el mercado en el pasado reciente (en los últimos 30 días).

CONCEPTOS :

Prima de Riesgo de Volatilidad

La Prima de Riesgo de Volatilidad (V-R-P) es la noción de que la Volatilidad Implícita (IV) tiende a ser más alta que la Volatilidad Realizada (HV) ya que los participantes del mercado tienden a sobrestimar la probabilidad de una caída significativa del mercado.

Esta sobreestimación puede explicar un aumento en la demanda de opciones como protección contra una cartera de acciones. Básicamente, esta mayor percepción de riesgo puede conducir a una mayor disposición a pagar por estas opciones para cubrir una cartera.

En otras palabras, los inversores están dispuestos a pagar una prima por las opciones para tener protección contra caídas significativas del mercado, incluso si estadísticamente la probabilidad de estas caídas es menor o insignificante.

Por lo tanto, la tendencia de la Volatilidad Implícita es de ser mayor que la Volatilidad Realizada, por lo cual el V-R-P es positivo.

Volatilidad Realizada/Histórica

La Volatilidad Histórica (HV) es la medida estadística de la dispersión de los rendimientos de un índice durante un período de tiempo determinado.

La Volatilidad Histórica es un concepto bien conocido en finanzas, pero existe confusión sobre cómo se calcula exactamente. Varias fuentes pueden usar fórmulas de Volatilidad Histórica ligeramente diferentes.

Para calcular la Volatilidad Histórica, utilicé el enfoque más común: desviación estándar anualizada de rendimientos logarítmicos, basada en los precios de cierre diarios.

Volatilidad Implícita

La Volatilidad Implícita (IV) es la previsión del mercado de un posible movimiento en el precio del índice y se expresa anualizada, utilizando porcentajes y desviaciones estándar en un horizonte de tiempo específico (generalmente 30 días).

IV se utiliza para cotizar contratos de opciones donde la alta Volatilidad Implícita da como resultado opciones con primas más altas y viceversa. Además, la oferta y la demanda de opciones y el valor temporal son factores determinantes importantes para calcular la Volatilidad Implícita.

La Volatilidad Implícita generalmente aumenta en los mercados bajistas y disminuye cuando el mercado es alcista.

Para determinar la Volatilidad Implícita de GOLD y SILVER utilicé sus índices de volatilidad: GVZ y VXSLV (30 días IV) proporcionados por CBOE.

Precaución

Tenga en cuenta que debido a que CBOE no proporciona datos en tiempo real en Tradingview, mi cálculo de V-R-P también se retrasa, y por este motivo no se recomienda usar en los primeros 15 minutos desde la apertura.

Este indicador está calibrado para un marco de tiempo diario.

Volatility Risk Premium (VRP) 1.0ENGLISH

This indicator (V-R-P) calculates the (one month) Volatility Risk Premium for S&P500 and Nasdaq-100.

V-R-P is the premium hedgers pay for over Realized Volatility for S&P500 and Nasdaq-100 index options.

The premium stems from hedgers paying to insure their portfolios, and manifests itself in the differential between the price at which options are sold (Implied Volatility) and the volatility the S&P500 and Nasdaq-100 ultimately realize (Realized Volatility).

I am using 30-day Implied Volatility (IV) and 21-day Realized Volatility (HV) as the basis for my calculation, as one month of IV is based on 30 calendaristic days and one month of HV is based on 21 trading days.

At first, the indicator appears blank and a label instructs you to choose which index you want the V-R-P to plot on the chart. Use the indicator settings (the sprocket) to choose one of the indices (or both).

Together with the V-R-P line, the indicator will show its one year moving average within a range of +/- 15% (which you can change) for benchmarking purposes. We should consider this range the “normalized” V-R-P for the actual period.

The Zero Line is also marked on the indicator.

Interpretation

When V-R-P is within the “normalized” range, … well... volatility and uncertainty, as it’s seen by the option market, is “normal”. We have a “premium” of volatility which should be considered normal.

When V-R-P is above the “normalized” range, the volatility premium is high. This means that investors are willing to pay more for options because they see an increasing uncertainty in markets.

When V-R-P is below the “normalized” range but positive (above the Zero line), the premium investors are willing to pay for risk is low, meaning they see decreasing uncertainty and risks in the market, but not by much.

When V-R-P is negative (below the Zero line), we have COMPLACENCY. This means investors see upcoming risk as being lower than what happened in the market in the recent past (within the last 30 days).

CONCEPTS:

Volatility Risk Premium

The volatility risk premium (V-R-P) is the notion that implied volatility (IV) tends to be higher than realized volatility (HV) as market participants tend to overestimate the likelihood of a significant market crash.

This overestimation may account for an increase in demand for options as protection against an equity portfolio. Basically, this heightened perception of risk may lead to a higher willingness to pay for these options to hedge a portfolio.

In other words, investors are willing to pay a premium for options to have protection against significant market crashes even if statistically the probability of these crashes is lesser or even negligible.

Therefore, the tendency of implied volatility is to be higher than realized volatility, thus V-R-P being positive.

Realized/Historical Volatility

Historical Volatility (HV) is the statistical measure of the dispersion of returns for an index over a given period of time.

Historical volatility is a well-known concept in finance, but there is confusion in how exactly it is calculated. Different sources may use slightly different historical volatility formulas.

For calculating Historical Volatility I am using the most common approach: annualized standard deviation of logarithmic returns, based on daily closing prices.

Implied Volatility

Implied Volatility (IV) is the market's forecast of a likely movement in the price of the index and it is expressed annualized, using percentages and standard deviations over a specified time horizon (usually 30 days).

IV is used to price options contracts where high implied volatility results in options with higher premiums and vice versa. Also, options supply and demand and time value are major determining factors for calculating Implied Volatility.

Implied Volatility usually increases in bearish markets and decreases when the market is bullish.

For determining S&P500 and Nasdaq-100 implied volatility I used their volatility indices: VIX and VXN (30-day IV) provided by CBOE.

Warning

Please be aware that because CBOE doesn’t provide real-time data in Tradingview, my V-R-P calculation is also delayed, so you shouldn’t use it in the first 15 minutes after the opening.

This indicator is calibrated for a daily time frame.

ESPAŇOL

Este indicador (V-R-P) calcula la Prima de Riesgo de Volatilidad (de un mes) para S&P500 y Nasdaq-100.

V-R-P es la prima que pagan los hedgers sobre la Volatilidad Realizada para las opciones de los índices S&P500 y Nasdaq-100.

La prima proviene de los hedgers que pagan para asegurar sus carteras y se manifiesta en el diferencial entre el precio al que se venden las opciones (Volatilidad Implícita) y la volatilidad que finalmente se realiza en el S&P500 y el Nasdaq-100 (Volatilidad Realizada).

Estoy utilizando la Volatilidad Implícita (IV) de 30 días y la Volatilidad Realizada (HV) de 21 días como base para mi cálculo, ya que un mes de IV se basa en 30 días calendario y un mes de HV se basa en 21 días de negociación.

Al principio, el indicador aparece en blanco y una etiqueta le indica que elija qué índice desea que el V-R-P represente en el gráfico. Use la configuración del indicador (la rueda dentada) para elegir uno de los índices (o ambos).

Junto con la línea V-R-P, el indicador mostrará su promedio móvil de un año dentro de un rango de +/- 15% (que puede cambiar) con fines de evaluación comparativa. Deberíamos considerar este rango como el V-R-P "normalizado" para el período real.

La línea Cero también está marcada en el indicador.

Interpretación

Cuando el V-R-P está dentro del rango "normalizado",... bueno... la volatilidad y la incertidumbre, como las ve el mercado de opciones, es "normal". Tenemos una “prima” de volatilidad que debería considerarse normal.

Cuando V-R-P está por encima del rango "normalizado", la prima de volatilidad es alta. Esto significa que los inversores están dispuestos a pagar más por las opciones porque ven una creciente incertidumbre en los mercados.

Cuando el V-R-P está por debajo del rango "normalizado" pero es positivo (por encima de la línea Cero), la prima que los inversores están dispuestos a pagar por el riesgo es baja, lo que significa que ven una disminución, pero no pronunciada, de la incertidumbre y los riesgos en el mercado.

Cuando V-R-P es negativo (por debajo de la línea Cero), tenemos COMPLACENCIA. Esto significa que los inversores ven el riesgo próximo como menor que lo que sucedió en el mercado en el pasado reciente (en los últimos 30 días).

CONCEPTOS:

Prima de Riesgo de Volatilidad

La Prima de Riesgo de Volatilidad (V-R-P) es la noción de que la Volatilidad Implícita (IV) tiende a ser más alta que la Volatilidad Realizada (HV) ya que los participantes del mercado tienden a sobrestimar la probabilidad de una caída significativa del mercado.

Esta sobreestimación puede explicar un aumento en la demanda de opciones como protección contra una cartera de acciones. Básicamente, esta mayor percepción de riesgo puede conducir a una mayor disposición a pagar por estas opciones para cubrir una cartera.

En otras palabras, los inversores están dispuestos a pagar una prima por las opciones para tener protección contra caídas significativas del mercado, incluso si estadísticamente la probabilidad de estas caídas es menor o insignificante.

Por lo tanto, la tendencia de la Volatilidad Implícita es de ser mayor que la Volatilidad Realizada, por lo cual el V-R-P es positivo.

Volatilidad Realizada/Histórica

La Volatilidad Histórica (HV) es la medida estadística de la dispersión de los rendimientos de un índice durante un período de tiempo determinado.

La Volatilidad Histórica es un concepto bien conocido en finanzas, pero existe confusión sobre cómo se calcula exactamente. Varias fuentes pueden usar fórmulas de Volatilidad Histórica ligeramente diferentes.

Para calcular la Volatilidad Histórica, utilicé el enfoque más común: desviación estándar anualizada de rendimientos logarítmicos, basada en los precios de cierre diarios.

Volatilidad Implícita

La Volatilidad Implícita (IV) es la previsión del mercado de un posible movimiento en el precio del índice y se expresa anualizada, utilizando porcentajes y desviaciones estándar en un horizonte de tiempo específico (generalmente 30 días).

IV se utiliza para cotizar contratos de opciones donde la alta Volatilidad Implícita da como resultado opciones con primas más altas y viceversa. Además, la oferta y la demanda de opciones y el valor temporal son factores determinantes importantes para calcular la Volatilidad Implícita.

La Volatilidad Implícita generalmente aumenta en los mercados bajistas y disminuye cuando el mercado es alcista.

Para determinar la Volatilidad Implícita de S&P500 y Nasdaq-100 utilicé sus índices de volatilidad: VIX y VXN (30 días IV) proporcionados por CBOE.

Precaución

Tenga en cuenta que debido a que CBOE no proporciona datos en tiempo real en Tradingview, mi cálculo de V-R-P también se retrasa, y por este motivo no se recomienda usar en los primeros 15 minutos desde la apertura.

Este indicador está calibrado para un marco de tiempo diario.

Wyckoff Method - Comprehensive Analysis# WYCKOFF METHOD - QUICK REFERENCE CHEAT SHEET

## 🟢 STRONGEST BUY SIGNALS

### 1. SPRING ⭐⭐⭐⭐⭐

- **What:** False breakdown below support on LOW volume

- **Look for:** Quick reversal, close above support

- **Entry:** When price closes back in range

- **Stop:** Below spring low

- **Target:** Top of range minimum

### 2. SOS (Sign of Strength) ⭐⭐⭐⭐

- **What:** Breakout above resistance on HIGH volume

- **Look for:** Wide spread up bar, strong close

- **Entry:** On breakout or wait for LPS pullback

- **Stop:** Below range top

- **Target:** Height of range projected up

### 3. SHAKEOUT ⭐⭐⭐⭐

- **What:** Sharp move below support with HIGH volume, immediate reversal

- **Look for:** Long lower wick, closes strong

- **Entry:** When price reclaims support

- **Stop:** Below shakeout low

- **Target:** Previous resistance

---

## 🔴 STRONGEST SELL SIGNALS

### 1. UTAD (Upthrust After Distribution) ⭐⭐⭐⭐⭐

- **What:** False breakout above resistance, quick rejection

- **Look for:** Spike high, weak close, often high volume

- **Entry:** When price closes back in range

- **Stop:** Above UTAD high

- **Target:** Bottom of range minimum

### 2. SOW (Sign of Weakness) ⭐⭐⭐⭐

- **What:** Breakdown below support on HIGH volume

- **Look for:** Wide spread down bar, weak close

- **Entry:** On breakdown or wait for LPSY rally

- **Stop:** Above range bottom

- **Target:** Height of range projected down

### 3. UPTHRUST ⭐⭐⭐⭐

- **What:** Move above resistance on LOW volume, weak close

- **Look for:** Long upper wick, closes in lower half

- **Entry:** When resistance holds

- **Stop:** Above upthrust high

- **Target:** Support level

---

## 📊 ACCUMULATION PHASES (Bottom Formation)

```

PHASE A: Stopping the Downtrend

├─ PS (Preliminary Support) - First buying

├─ SC (Selling Climax) - Panic bottom ⚠️ KEY EVENT

├─ AR (Automatic Rally) - Relief bounce

└─ ST (Secondary Test) - Retest SC low

PHASE B: Building the Cause

├─ Trading range forms

├─ Multiple tests of support

├─ Volume decreasing

└─ Absorption occurring

PHASE C: The Test

├─ SPRING - False breakdown ⚠️ KEY EVENT

└─ TEST - Support holds on low volume

PHASE D: Dominance Emerges

├─ SOS - Breakout ⚠️ KEY EVENT

├─ LPS - Last Point of Support (pullback)

└─ BU - Backup

PHASE E: Markup

└─ New uptrend, strong momentum

```

**Background Color:** Blue → Green (getting brighter)

**Action:** Buy in Phase C/D, Hold through Phase E

---

## 📊 DISTRIBUTION PHASES (Top Formation)

```

PHASE A: Stopping the Uptrend

├─ PSY (Preliminary Supply) - First selling

├─ BC (Buying Climax) - Euphoric top ⚠️ KEY EVENT

├─ AR (Automatic Reaction) - Sharp drop

└─ ST (Secondary Test) - Retest BC high

PHASE B: Building the Cause

├─ Trading range forms

├─ Multiple tests of resistance

├─ Demand being absorbed

└─ Volume patterns change

PHASE C: The Test

└─ UTAD - False breakout ⚠️ KEY EVENT

PHASE D: Dominance Emerges

├─ SOW - Breakdown ⚠️ KEY EVENT

└─ LPSY - Last Point of Supply (rally to exit)

PHASE E: Markdown

└─ New downtrend, strong selling

```

**Background Color:** Orange → Red (getting darker)

**Action:** Sell in Phase C/D, Stay out during Phase E

---

## 💰 VOLUME SPREAD ANALYSIS (VSA)

| Signal | Meaning | Color | Implication |

|--------|---------|-------|-------------|

| **ND** (No Demand) | Up bar, LOW volume | 🟠 Orange | Weakness - uptrend ending |

| **NS** (No Supply) | Down bar, LOW volume | 🔵 Blue | Strength - downtrend ending |

| **SV** (Stopping Volume) | VERY HIGH volume, narrow spread | 🟣 Purple | Potential reversal |

| **UT** (Upthrust) | Above resistance, LOW vol, weak close | 🔴 Red | Sell signal |

| **SO** (Shakeout) | Below support, HIGH vol, strong close | 🟢 Green | Buy signal |

---

## 🎯 VOLUME INTERPRETATION

| Volume Level | Bar Color | Meaning |

|--------------|-----------|---------|

| **VERY HIGH** (>2x average) | Dark Green/Red | Climax, potential reversal |

| **HIGH** (>1.5x average) | Light Green/Red | Strong interest |

| **NORMAL** | Gray | Average trading |

| **LOW** (<0.7x average) | Faint Gray | Testing, no interest |

---

## ⚖️ EFFORT vs RESULT

| Scenario | Volume | Spread | Meaning |

|----------|--------|--------|---------|

| **High Effort, Low Result** | HIGH | Narrow | ⚠️ Potential reversal |

| **Low Effort, High Result** | LOW | Wide | ⚠️ Trend weakening |

| **High Effort, High Result** | HIGH | Wide | ✅ Strong trend |

| **Low Effort, Low Result** | LOW | Narrow | 😴 No interest |

---

## 📏 TRADING RULES

### ✅ DO:

- ✅ Wait for confirmation before entering

- ✅ Trade in direction of higher timeframe

- ✅ Use springs and UTAD as primary signals

- ✅ Measure trading range for targets

- ✅ Place stops outside the range

- ✅ Look for volume confirmation

- ✅ Check multiple timeframes

- ✅ Focus on Phase C and D events

### ❌ DON'T:

- ❌ Buy during Phase E Markdown

- ❌ Sell during Phase E Markup

- ❌ Trade against major trend

- ❌ Ignore volume signals

- ❌ Enter without clear stop loss

- ❌ Trade every signal

- ❌ Use on very low timeframes without practice

- ❌ Ignore the context

---

## 🎪 COMPOSITE OPERATOR (Smart Money)

### 💰 Green Money Symbol (Bottom)

- **Meaning:** Institutions accumulating

- **Location:** Demand zones, springs, tests

- **Action:** Follow the smart money - buy

### 💰 Red Money Symbol (Top)

- **Meaning:** Institutions distributing

- **Location:** Supply zones, UTAD, weak rallies

- **Action:** Follow the smart money - sell

---

## 📍 SUPPLY & DEMAND ZONES

### 🟢 Demand Zones (Green Boxes)

- **Created at:** SC, Spring, Shakeout

- **Represents:** Where smart money bought

- **Action:** Look for bounces

### 🔴 Supply Zones (Red Boxes)

- **Created at:** BC, UTAD, Upthrust

- **Represents:** Where smart money sold

- **Action:** Look for rejections

---

## 🎯 TARGET CALCULATION

### Measured Move Method

```

1. Measure trading range height

Example: Top at 120, Bottom at 100 = 20 points

2. Add to breakout point (accumulation)

Breakout at 120 + 20 = Target: 140

3. Or subtract from breakdown (distribution)

Breakdown at 100 - 20 = Target: 80

```

### Multiple Targets

- **Conservative:** 1x range height (100% probability reached)

- **Moderate:** 1.5x range height (70% probability)

- **Aggressive:** 2x range height (40% probability)

---

## ⏰ TIMEFRAME GUIDE

| Timeframe | Use For | Reliability | Recommended For |

|-----------|---------|-------------|-----------------|

| **Weekly** | Major trends | ⭐⭐⭐⭐⭐ | Position traders |

| **Daily** | Swing trades | ⭐⭐⭐⭐⭐ | Most traders |

| **4-Hour** | Active swing | ⭐⭐⭐⭐ | Active traders |

| **1-Hour** | Day trading | ⭐⭐⭐ | Experienced only |

| **15-Min** | Scalping | ⭐⭐ | Experts only |

**Golden Rule:** Always check one timeframe higher for context!

---

## 🚨 ALERT PRIORITY

### 🔔 MUST-HAVE ALERTS

1. Spring

2. UTAD

3. SOS

4. SOW

### 🔔 NICE-TO-HAVE ALERTS

5. Selling Climax (SC)

6. Buying Climax (BC)

7. Smart Money Accumulation

8. Smart Money Distribution

### 🔔 CONFIRMATION ALERTS

9. Phase E Markup

10. Phase E Markdown

---

## 💡 QUICK DECISION TREE

```

Is there a clear trading range?

├─ YES

│ ├─ Did price break BELOW support?

│ │ ├─ Volume LOW + Quick reversal = SPRING → BUY ✅

│ │ └─ Volume HIGH + Stays down = Breakdown → SELL ⚠️

│ │

│ └─ Did price break ABOVE resistance?

│ ├─ Volume LOW + Quick reversal = UTAD → SELL ✅

│ └─ Volume HIGH + Stays up = Breakout → BUY ⚠️

│

└─ NO

├─ Strong uptrend = Wait for re-accumulation

└─ Strong downtrend = Wait for re-distribution

```

---

## 📝 PRE-TRADE CHECKLIST

Before entering any trade:

- Identified the current Wyckoff phase

- Confirmed with volume analysis

- Checked higher timeframe trend

- Located supply/demand zones

- Identified clear entry point

- Set stop loss level

- Calculated target (risk:reward >1:2)

- Verified position size (risk 1-2%)

- Have at least 2 confirming signals

- Not trading against major trend

---

## 🧠 REMEMBER

**The Three Laws:**

1. **Supply & Demand** - Price is determined by imbalance

2. **Cause & Effect** - Range size predicts move size

3. **Effort & Result** - Volume should confirm price movement

**The Key Principle:**

> "Trade with the Composite Operator (smart money), not against them"

**Best Setups:**

1. Spring in accumulation (Phase C)

2. UTAD in distribution (Phase C)

3. SOS breakout (Phase D)

4. SOW breakdown (Phase D)

**When in Doubt:**

- ❓ Stay out

- 📈 Use higher timeframe

- 📚 Review the documentation

- 🎯 Wait for clearer signal

---

## 📱 INDICATOR SETTINGS QUICK SETUP

**For Stocks/Crypto (Good Volume Data):**

- Volume MA Length: 20

- High Volume Multiplier: 1.5

- Climax Volume: 2.0

- Swing Length: 5

**For Forex (Limited Volume Data):**

- Volume MA Length: 20

- High Volume Multiplier: 1.3

- Climax Volume: 1.8

- Swing Length: 7

- Turn OFF "Volume Confirmation"

**For Day Trading:**

- Swing Length: 3

- All other settings: Default

**For Position Trading:**

- Swing Length: 7-10

- Volume MA Length: 30

- Use Daily/Weekly charts

---

## 🎓 SKILL PROGRESSION

### Beginner (Month 1-2)

- Focus on: SC, Spring, SOS

- Timeframe: Daily only

- Goal: Identify phases correctly

### Intermediate (Month 3-6)

- Add: All accumulation events

- Timeframe: Daily + 4H

- Goal: Trade springs profitably

### Advanced (Month 6-12)

- Add: Distribution events, VSA

- Timeframe: Multiple timeframes

- Goal: Trade complete cycles

### Expert (Year 2+)

- Master: All events, all timeframes

- Combine: With other methodologies

- Goal: Consistent profitability

---

**Print this sheet and keep it next to your trading desk!**

*Remember: Quality over quantity. Wait for the best setups.*

# Wyckoff Method - Comprehensive Analysis Indicator

## Complete Implementation Guide for TradingView Pine Script

---

## TABLE OF CONTENTS

1. (#overview)

2. (#installation)

3. (#theory)

4. (#components)

5. (#signals)

6. (#strategies)

7. (#settings)

8. (#alerts)

9. (#patterns)

10. (#troubleshooting)

---

## OVERVIEW

This indicator implements Richard Wyckoff's complete trading methodology, including:

- **All 5 Phases** of Accumulation and Distribution

- **18+ Wyckoff Events** (PS, SC, AR, ST, Spring, SOS, LPS, BC, UTAD, SOW, etc.)

- **Volume Spread Analysis (VSA)** principles

- **Supply & Demand Zone** detection

- **Composite Operator** logic (Smart Money tracking)

- **Effort vs Result** analysis

- **Three Wyckoff Laws**: Supply/Demand, Cause/Effect, Effort/Result

---

## INSTALLATION

### Step 1: Copy the Code

1. Open the `wyckoff_comprehensive.pine` file

2. Select all code (Ctrl+A / Cmd+A)

3. Copy to clipboard (Ctrl+C / Cmd+C)

### Step 2: Add to TradingView

1. Go to TradingView.com

2. Open any chart

3. Click "Pine Editor" at the bottom of the screen

4. Click "New" or "Open"

5. Paste the entire code

6. Click "Save" and give it a name

7. Click "Add to Chart"

### Step 3: Verify Installation

You should see:

- Labels on the chart (PS, SC, Spring, SOS, etc.)

- Background colors indicating phases

- Volume analysis in the lower pane

- A table in the top-right corner showing current phase

---

## WYCKOFF METHOD THEORY

### The Three Fundamental Laws

#### 1. **Law of Supply and Demand**

- Price rises when demand exceeds supply

- Price falls when supply exceeds demand

- The indicator tracks volume vs price movement to identify imbalances

#### 2. **Law of Cause and Effect**

- A period of accumulation (cause) leads to markup (effect)

- A period of distribution (cause) leads to markdown (effect)

- Trading ranges build "cause" for future price movement

#### 3. **Law of Effort vs Result**

- **Effort** = Volume (energy put into the market)

- **Result** = Price movement (spread of the bar)

- High effort with low result = potential reversal

- Low effort with high result = trend weakness

### The Five Phases

#### **ACCUMULATION CYCLE**

**Phase A: Stopping the Downtrend**

- Preliminary Support (PS): First sign of buying

- Selling Climax (SC): Panic selling exhaustion

- Automatic Rally (AR): Bounce from SC

- Secondary Test (ST): Test of SC low on lower volume

**Phase B: Building the Cause**

- Trading range develops

- Supply being absorbed by composite operator

- Multiple tests of support and resistance

- Volume generally decreases

**Phase C: The Test (Spring)**

- False breakdown below support

- Traps late sellers

- Quick reversal on low volume

- Last chance to accumulate before markup

**Phase D: Dominance Emerges**

- Sign of Strength (SOS): Break above resistance

- Last Point of Support (LPS): Pullback opportunity

- Backup (BU): Final consolidation

- Demand clearly exceeds supply

**Phase E: Markup**

- New uptrend established

- Price moves rapidly higher

- Phase E can last months/years

- Original trading range becomes support

#### **DISTRIBUTION CYCLE**

**Phase A: Stopping the Uptrend**

- Preliminary Supply (PSY): First sign of selling

- Buying Climax (BC): Euphoric buying exhaustion

- Automatic Reaction (AR): Sharp selloff from BC

- Secondary Test (ST): Test of BC high on lower volume

**Phase B: Building the Cause**

- Trading range at top

- Demand being absorbed by composite operator

- Multiple tests of support and resistance

**Phase C: The Test (UTAD)**

- Upthrust After Distribution

- False breakout above resistance

- Traps late buyers

- Quick reversal

**Phase D: Dominance Emerges**

- Sign of Weakness (SOW): Break below support

- Last Point of Supply (LPSY): Rally opportunity to exit

- Supply clearly exceeds demand

**Phase E: Markdown**

- New downtrend established

- Price moves rapidly lower

- Original trading range becomes resistance

---

## INDICATOR COMPONENTS

### 1. EVENT LABELS

#### Accumulation Events (Green labels)

- **PS** = Preliminary Support

- **SC** = Selling Climax (largest label, most important)

- **AR** = Automatic Rally

- **ST** = Secondary Test

- **SPRING** = Spring (critical buy signal)

- **TEST** = Test of support

- **SOS** = Sign of Strength (breakout)

- **LPS** = Last Point of Support

- **BU** = Backup

#### Distribution Events (Red labels)

- **PSY** = Preliminary Supply

- **BC** = Buying Climax (largest label, most important)

- **AR** = Automatic Reaction

- **ST** = Secondary Test

- **UTAD** = Upthrust After Distribution (critical sell signal)

- **SOW** = Sign of Weakness

- **LPSY** = Last Point of Supply

#### VSA Events (Small colored labels)

- **ND** (Orange) = No Demand - weakness

- **NS** (Blue) = No Supply - strength

- **SV** (Purple) = Stopping Volume

- **UT** (Red) = Upthrust - weakness

- **SO** (Green) = Shakeout - strength

#### Composite Operator (💰 symbols)

- Green 💰 at bottom = Smart Money Accumulation

- Red 💰 at top = Smart Money Distribution

### 2. BACKGROUND COLORS

- **Light Blue** = Phase A (Accumulation)